The use of established technology in achieving social good and the sustainable development goals can be generally accepted, but the question of whether blockchain, as a specific and emerging technology, can contribute to the goals is at very early stages of investigation. We should be aware of the risk of blockchain as ‘a solution in search of a problem’ and of being drawn into the hype surrounding its use and efficacy. In support of the use of blockchain, there are opinions that blockchain “has more near-term potential for social impact than originally thought” (Calvert, 2018), and that new technologies being deployed in developing countries means not having the legacy of existing technologies which can hinder adoption. Of the seventeen goals, some lend themselves more appropriately to, and could benefit more greatly from, using blockchain and distributed ledger technologies.

The World Food Programme has delivered blockchain solutions that contribute to achieving Goal 2: Zero hunger. The programme distributes cash to 28 million people in 64 countries (WFP, 2021) but recognised that in some countries the existing financial solutions were insufficient, unreliable and incurred high transaction fees. The Building Blocks project implemented a private, permissioned blockchain to record transactions made by people purchasing groceries which reduced financial transaction fees and ensured greater security and privacy.

The WFP’s project provides an example of how blockchain can be used in tackling a very specific problem; that of people in refugee camps purchasing food without concerns of centralised third-parties having access to their personal data or losing food vouchers. In this case, it could be argued that blockchain solves more problems for the organisation than it does for its beneficiaries, as it reduces the transaction fees the organisation pays and provides more accurate data about those using the system. Based on this example we can conclude that blockchain can have a role to play in achieving the goal of zero hunger but has a long way to go before that contribution can be considered significant.

Goal 8: Decent work and economic growth, is another goal that blockchain could contribute to. For the 2 billion ‘unbanked’ people in the world, not having access to financial services hinders the economic growth of individuals, families, towns, and entire countries. According to the central bank of Sierra Leone, over three-quarters of the country’s population does not access formal financial services (Ledger Insights, 2019). In an attempt to tackle this issue and so enable economic growth, the charity Kiva set up a blockchain solution to provide microloans to people who are unable to provide a credit history due to their unbanked status. Kiva reports on the impact of its service as an overall but it is difficult to measure the success of the blockchain technologies, either in comparison to a different solution or in achieving the sustainable development goal of “sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all” (UN, 2021).

Blockchain technologies, among other emerging technologies, have much potential in contributing to achieving the sustainable development goals but must be approached cautiously and with consideration for the unintended consequences the introduction of new technologies can have. The use of blockchain technology can contribute to specific parts of solutions that contribute to achieving the Sustainable Development Goals but to suggest that a technology such as blockchain can achieve a goal alone would risk straying into more hype than reality.

In tackling some of these issues, the Blockchain Commission for Sustainable Development was set up in 2017 to “develop a multi-sectoral framework to support the UN system, along with Member States, intergovernmental organizations, the private sector and civil society in utilizing blockchain-based technologies to develop local, national and global solutions to urgent challenges.” (IISD, 2018). The IISD works to help other organisations better understand blockchain and it’s real world applications, including aspects such as how blockchain fits within a country’s legislation and telecoms infrastructure. These challenges are important to understand when considering how blockchain can contribute to achieving the sustainable development goals as the question becomes less about the application of blockchain technology and more about how to build the national and international infrastructure that would be necessary for blockchain to be implemented in order for it to contribute to the goals.

References

Calvert, D. (2018). Can Blockchain Be Used for Public Good? Stanford Business.

International Institute for Sustainable Development. (2018). Commission White Paper Explores Blockchain Use for SDGs. sdg.iisd.org

Ledger Insights. (2019). Kiva sets up Sierra Leone blockchain ID system. ledgerinsights.com

United Nations. (2021). The 17 Goals. sdgs.un.org

World Food Programme. (201). Building Blocks: Blockchain for Zero Hunger. innovation.wfp.org

The logistics and supply chain sector is undergoing technology-driven digital transformation where emerging technologies result in a strategic response that adapts the way companies create value (Vial, 2019). This technology-push model of innovation (Rothwell, 1994) where emerging technologies are developed without a clear use case in mind and then adopted horizontally across sectors leads to the convergence of complementary technology vertically within a sector. In the logistics and supply chain sector the convergence between the Internet of Things providing the data production layer and Blockchain and DLT providing the data exchange layer enables new means of value creation for firms.

Blockchain and Distributed Ledger Technologies have particular applicability to global logistics and supply chain management as many different companies are involved in the processes of shipping and require accurate, timely and trusted data in order to conduct their operations efficiently. All of the firms accessing the data on the blockchain can trust that it is immutable, has been arrived at through consensus of the other nodes in the network, that is the other firms in the supply chain ecosystem, and has absolute auditability. Being able to trust in the data rather than rely on established business relationships offers the potential of all firms involved to establish different kinds of business relationships where firms provide business-to-business services without the need for existing business practices of price negotiation and written contracts.

Wang et al (2019) list four areas where blockchain technologies and the increased trust they provide has benefits in the logistics industry: “extended visibility and traceability, supply chain digitalisation and disintermediation, improved data security and smart contracts.” Extended visibility and traceability is a result of the trust enabled by the use of an immutable data ledger such as blockchain. With an average of 1,382 shipping containers lost at sea each year (BIFA, 2020), the ability of shipping firms to have accurate and up-to-date data about lost cargo enables them to work more effectively with manufacturers and insurance companies. EY is exploring blockchain-enabled insurance solutions, “because marine insurance is a complex international ecosystem, with multiple parties, multiple jurisdictions, high transaction volumes and significant levels of reconciliation.” (EY, 2017). The high degree of trust required in order to process insurance claims of the value and complexity that EY handles relies on multiple human processes that involve investigation and approval, processes that would become redundant if using a single, trusted, and immutable source of data in support of insurance claims and processing.

The use of smart contracts aims to reduce complexity in a supply chain by automating business transactions that rely on the verification of predetermined conditions and the execution of agreements written into the code of the smart contract. ShipChain is a logistics utility ecosystem using blockchain technology to provide smart contracts that enable “trustless contract execution, historical data immutability, and no single point of failure.” (Shipchain, 2021). The solution provides greater visibility of delivery hand-offs and so reduces loss and theft whilst enabling the transactions written into smart contracts to be executed as a delivery takes place.

IBM estimates that the cost of trade documentation is approximately one fifth the cost of shipping physical goods (IBM, 2018). This makes the cost of moving information between exporters, freight forwarders, ports and terminals, ocean carriers, authorities, transportation management and importers in the billions of dollars a year. And this does not include the ancillary costs of the data entry for good manufactures, insurance processes, etc. By providing a single trusted source of data, blockchain can reduce these transaction costs (Schmidt & Wagner, 2019) and increase profitability across the sector.

Although blockchain and distributed ledger technologies stand to offer considerable benefits to the entire logistics and supply chain sector, they do not come without risks and challenges. The introduction of new technologies into a business is a costly endeavour that risks pushing out smaller firms that are unable to invest in such infrastructure as quickly as larger firms. The use of smart contracts, for example, relies on the coding of the contract to be well-defined, deterministic, and visible to all parties, and although referred to as ‘contracts’, smart contracts are not legally enforceable (Kruse et al, 2020).

In summary, logistics and supply chain companies are increasingly exploring Blockchain and DLT as part of the digital transformation of the sector, and to enable faster and more accurate data exchange between all companies within the supply chain to increase operational efficiency and reduce costs. Emerging technologies, including the Internet of Things and Distributed Ledger Technologies stand to introduce a great deal of change to the global logistics and supply chain industry.

References

British International Freight Association. (2020). Containers Lost At Sea – 2020 Update. bifa.org.

EY. (2017) Better-working insurance: moving blockchain from concept to reality. ey.com.

IBM. (2018). Digitizing Global Trade with Maersk and IBM. ibm.com

Kruse, C. J., Villa, J. C., Mileski, J. P. & Galvao, C. (2020). Analysis of Blockchain’s Impacts on and Applicability to the Maritime Industry – May 2019 to August 2020. Maritime Transportation Research and Education Center.

Rothwell, R. (1994). Towards the Fifth-generation Innovation Process. International Marketing Review, 11(1), 7-31.

Schmidt, C., G. & Wagner, S., M. (2019). Blockchain and supply chain relations: A transaction cost theory perspective. Journal of Purchasing and Supply Management. Volume 25, Issue 4, 2019.

Shipchain. (2012). The ShipChain Ecosystem. shipchain.io.

Vial, G. (2019) Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems, Volume 28, Issue 2.

Wang, Y., Han, J.H. and Beynon-Davies, P. (2019). Understanding blockchain technology for future supply chains: a systematic literature review and research agenda, Supply Chain Management, Vol. 24 No. 1, pp. 62-84.

It is generally accepted that emerging technologies act as enabling forces for economic, social, and business transformation (Cohen & Amorós, 2014; Paschen, Kietzmann, & Kietzmann, in press, in Morkunas et al, 2019). Morkunas et al (2019) predict that blockchain technologies will “challenge existing business models and offer opportunities for new value creation”, whilst the UK Government Chief Scientific Officer described distributed ledger technology as a “potential explosions of creative potential that catalyse exceptional levels of innovation“ that can “reform our financial markets, supply chains, consumer and business-to-business services, and publicly-held registers” (2016). If these predictions come to fruition then we can expect Distributed Ledger Technology and Blockchain to have considerable impact on business and the future of work.

This essay attempts to reach an answer to the question ‘What is the role of DLT and blockchain in the future of work?’ The question is explored through looking at recent literature for a definition of the future of work, how emerging technologies, specifically Distributed Ledger Technology and Blockchain, are expected to affect the nature of work, and which sectors are likely to be most impacted. The discussion considers examples of the use, issues and challenges for DLT and blockchain in the top three affected sectors. In drawing a conclusion about the role of DLT and Blockchain in the future of work I argue that emerging technologies have an amplified impact where more than just a single technology is applied, and that DLT and blockchain are likely to have a greater impact on some sectors than others.

Literature Review

What is the future of work?

Work in the 21st century is entering a Fourth Industrial Revolution, a revolution built on an increasing number of emerging and interacting technologies that is “more comprehensive and all-encompassing than anything we have ever seen” (Schwab & Samans, 2016). ‘The future of work’ is a current and ongoing debate about how every occupation in every sector is undergoing a fundamental transformation as a result of the impacts of emerging technologies and digital transformation. The debate is wide-ranging, with far-reaching consequences, spanning from the offer of benefits for employers and employees augmented by technology (Grabowski, 2018) to mass economic disruption from the loss of jobs (Ernst et al, 2019). While some jobs are threatened by redundancy and others grow rapidly, existing jobs are also going through a change in the skill sets required to do them (Schwab & Samans, 2016). Some sectors can expect greater change than others.

What factors will affect the future of work?

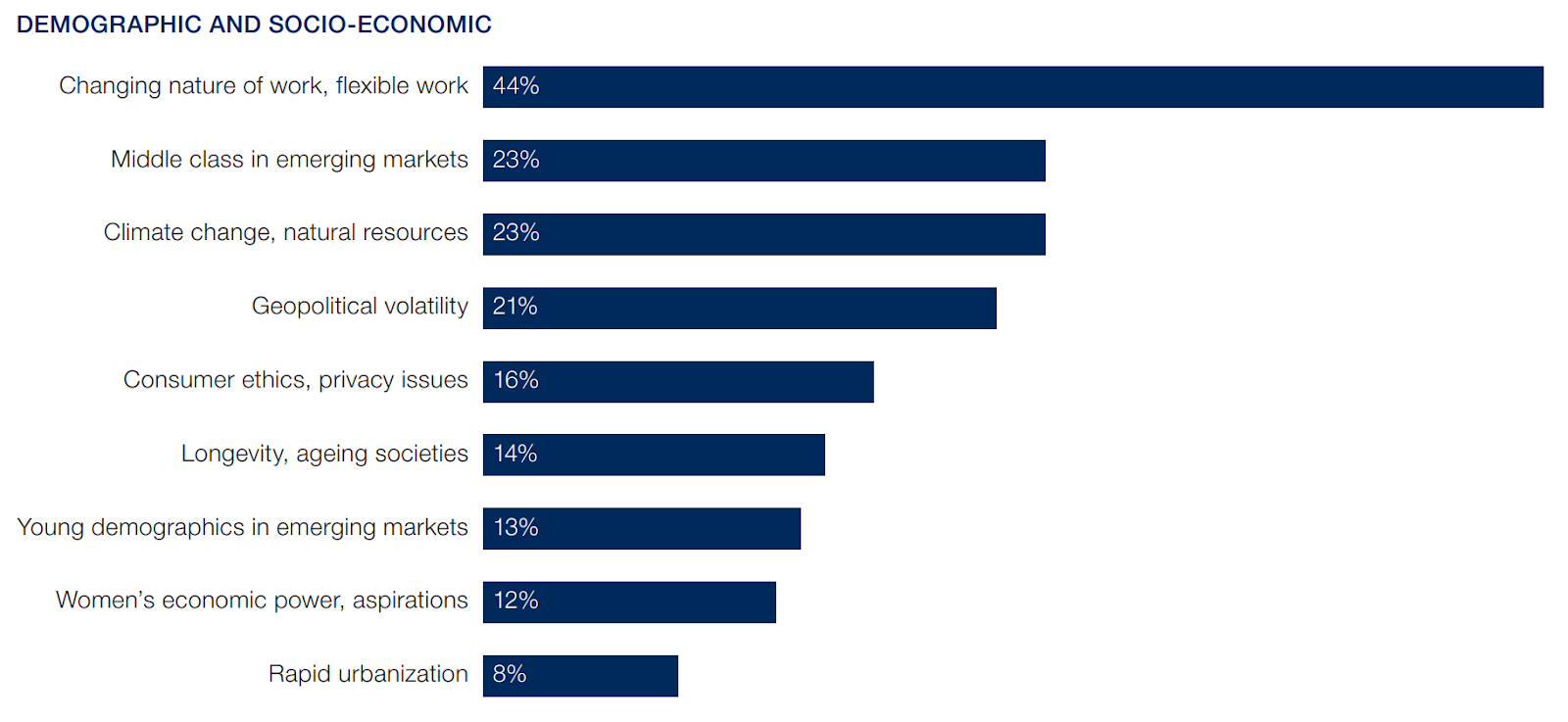

Along with the changes to work and working life brought about by technology there are wider trends such as globalisation of labour markets through the diffusion of outsourcing and offshoring, and job polarisation (Berg et al, 2018) that impact the future of work debate. For the purposes of this paper we cannot consider all of these factors and will instead focus on the potential impacts of emerging technologies in general, and Distributed Ledger Technologies and Blockchain specifically as we try to understand what role they may play in the future of work. However, one closely related trend that is worth discussing is the increase of flexible working arrangements as shown in Figure 1. The graph from the World Economic Forum shows 44% of respondents stated that the changing nature of work was the greatest driver for change across all industries. This matches with the findings from Berg et al (2018) where the two most important reasons for crowdworking were to “complement pay from other jobs” (32%) and because they “prefer to work from home” (22%). This suggests people are looking for more flexibility in their working life and turning to technology to enable it.

Figure 1: Demographic and socio-economic drivers of change, industries overall

Source: The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution, World Economic Forum.

Which technologies will affect the future of work?

The World Economic Forum report lists the nine technologies it’s respondents considered drivers of change (Fig. 2). Noticeably, DLT & Blockchain are not specifically listed as technologies that are expected to drive change. It could be argued that DLT & Blockchain technology has yet to achieve the maturity and adoption necessary for a study of this breadth to recognise its potential impact. This is backed-up by the British Standards Institution report which states the challenges of Blockchain adoption as including: “lack of clarity on the terminology and perceived immaturity of the technology, perceived risks in early adoption and likely disruption to existing industry practices, and insufficient evidence on business gains and wider economic impact” (Deshpande, 2017). DLT and Blockchain should be expected to impact the future of work, but perhaps those expectations are not arising just yet.

Figure 2: Technology drivers of change, industries overall

Source: The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution, World Economic Forum.

If Distributed Ledger Technologies and Blockchain are not yet impacting businesses and the future of work in a generic way like mobile and cloud are, then which specific industries are being affected by DLT and Blockchain?

Which sectors are likely to be most affected by Blockchain?

The Global Blockchain Benchmarking Study (Hileman & Rauchs, 2017) (Fig.3) shows how blockchain is at use by different industry sectors, with the banking & finance industry the highest user, followed by government & public goods, and then insurance. Those sectors which use Blockchain the most stand to be the most affected by its use, and so it is these sectors that we should expect DLT and blockchain to play more of a role in shaping the future of work.

Figure 3. Sectors currently using blockchain.

Source: Global Blockchain Benchmarking Study

Discussion

The following discussion looks at the role DLT and blockchain may play in the future of work in the top three sectors identified in the Global Blockchain Benchmarking Study, including examples and considering some of the challenges and issues.

Distributed Ledger Technology and Blockchain in the Banking and finance sector

The finance sector is being disrupted by DLT and blockchain (Buitenhek, 2016., Natarajan et al, 2017, Treleaven et al, 2017, Hassani et al, 2018). This seems undeniable. Blockchain technology serves a finance use case very well, offering as it does an immutable record of transactions and means of solving the double-spend problem (Nakamoto, 2008). Services such as Corda which “enables businesses in Banking, Capital Markets, Trade Finance, Insurance and beyond to transact directly and in strict privacy using smart contracts, reducing transaction and record-keeping costs and streamlining business operations” (Corda, 2021) demonstrate how large corporations in highly regulated industries are beginning to adopt blockchain technologies.

However, blockchain is not without its weaknesses of security, scalability, and efficiency (Dinh & Thai, 2018) which present considerable challenges in a banking and finance setting. Adoption of new technologies is always dependent on multiple factors, but perhaps it is precisely its disruptiveness that presents a challenge to the adoption of DLT and blockchain in the finance industry. As Tapscott and Tapscott (2017) state, the finance industry suffers from being “centralized, which makes it resistant to change… but the solution to this innovation logjam has emerged: blockchain.”

Let’s consider a case study of how one start-up is using blockchain to provide a disruptive microfinance solution.

Blockchain in Microfinance

“As the fintech landscape evolves at an unprecedented speed, Mastercard provides the infrastructure and assets to help fintech innovators grow and ultimately bring more people into the digital economy,” said Amy Neale, Senior Vice President, Fintech & Enablers. (Mastercard, 2021). One of those innovators is Brazil-based Moeda Seeds, a digital banking, payment and micro credit services powered by blockchain. “Since its founding in 2017, the company has used blockchain technology and has focused on the unbanked and under-banking population in Brazil“ (Moeda, 2021). They use blockchain technology to decrease lending costs, allowing microfinance lenders to send money directly to the recipients without the need for various middlemen (Hofer, 2018).

Microfinance Institutions, like Moeda, are organizations that provide small loans to borrowers who typically lack collateral, steady employment, or a verifiable credit history and therefore do not have access to traditional commercial banking (Coli et al, 2021). The use of Blockchain technology in microfinance introduces a number of benefits that are difficult to achieve through traditional financial institutions and technologies, including:

Transparency for investors to monitor repayments.

Reduced transaction fees by removing the need for intermediary organisations.

Builds an immutable and publicly available credit history for each lender (Adebaki, 2019).

In the case of Moeda, blockchain plays a role in the future of work for the Brazilian farmers, enabling them to fund their businesses without the need for traditional finance mechanisms such as capital or credit history.

Distributed Ledger Technology and Blockchain’s role in Government & Public Goods

Distributed Ledger Technologies and Blockchain have a role to play in government by performing a range of activities, including:

verification of documents such as licenses, proofs of records, transactions, processes or events such as birth of a child,

movement of assets such as transferring money from one entity to another after some work conditions are met,

asset ownership registers such as land registries, property titles and other types of ownership of physical assets and

management of identities like e-identities for citizens and city residents. (Ojo & Adebayo)

Blockchain can be used to address inefficiencies in government systems to increase the effectiveness of public service activities (Ojo & Adebayo). An example of this can be found in the Illinois Department of Innovation & Technology’s proof-of-concept for providing physicians with a means to obtain licenses to practice in multiple states. The Interstate Medical Licensure Compact, built on blockchain, not only offers advantages for the physicians but also strengthens public protection by enhancing the ability of states to share investigative and disciplinary information (Thomas, 2018).

The challenges around government departments adopting emerging technologies such as blockchain include justifying the use of public money and whether blockchain serves sufficient use cases. Estonia has been testing blockchain for limited use cases such as land registry to improve data integrity but has clearly stated that investment in other emerging technologies such as artificial intelligence is a greater priority (Govchain, 2019).

Distributed Ledger Technology and Blockchain in the insurance industry

DLT and blockchain continue to be explored in the insurance industry as a means of achieving the vision where “data is linked automatically to digital contracts which can trigger automated processes. Everyone trusts the accuracy of the data and can share it easily. World-class encryption provides the necessary security, and there’s a clear, immutable audit trail to underpin end-to-end underwriting and claims governance.” (EY, 2017). EY’s Insurwave, a blockchain enabled marine insurance product, aims to “deliver major gains in transparency, efficiency and auditability in the insurance value chain.” (EY, 2017). Replacing traditional databases with a blockchain creates immutable records allowing for better risk assessments on the part of insurers and quicker claims payouts for shippers. The operational efficiency gained by such solutions reduces the cost of moving information within and between companies. However, an issue to be faced by the insurance industry as a whole is how to work with regulators to ensure legal requirements and regulations evolve in line with new use cases for the technology. Clearly this is a policy issue rather than a technology one but could stand in the way of blockchain solutions becoming the standard across the insurance industry.

Conclusion

This essay started with a definition of the future of work debate as a response to emerging technologies and digital transformation, and considered which sectors are likely to be the most affected by the use of DLT & blockchain. The discussion looked at the use of blockchain in the finance sector, government and insurance industry, considering some current uses, challenges and opportunities. From looking at this we can draw the following conclusions:

DLT & blockchain will have a far greater role in changing some industries than it does in others. The effects will be greater in sectors where multiple organisations need access to the same data and for that data to be trusted as a single source of truth.

DLT & blockchain is likely to change the nature of the relationship between businesses, transforming aspects where a trust-based relationship exists. It has the potential to enable businesses to move away from centralised authorities.

All sectors and industries suffer similar challenges with the adoption of DLT & blockchain, including regulation, understanding and clearly defined use cases.

The effects on the future of work are likely to be considerably more profound where DLT & blockchain intersect with other emerging technology such as the Internet of Things and Artificial Intelligence.

Distributed ledger technologies and blockchain, as two of many emerging technologies, can be expected to have a contributory role in changing the future of work, and it’s clear how these technologies can be used in specific use cases, but it would be less prudent to conclude a general direct impact in the way that automation technologies, for example, can be expected to affect employment and the types of jobs available.

References

Adebaki, B. (2019). Microfinance and alternative data meets the world of Blockchain. Blockchain at Berkeley.

Berg, J., Furrer, M., Harmon, E., Rani, U. and Six Silberman, M. (2018). Digital labour platforms and the future of work: Towards decent work in the online world. International Labour Office – Geneva, ILO, 2018.

Buitenhek, M. (2016). Understanding and applying Blockchain technology in banking: Evolution or revolution? Journal of Digital Banking, Volume 1 / Number 2 / AUTUMN/FALL 2016, pp. 111-119(9).

CB Insights. (2021). Banking Is Only The Beginning: 58 Big Industries Blockchain Could Transform. CBInsights.com.

CB Insights. (2019). How Blockchain Could Disrupt Insurance. CBInsights.com.

Coli, P., Pflueger, C. & Campbell, T. (). Blockchain Uses for Microfinance Institutions in the Water and Sanitation Sector. Inter-American Development Bank.

Corda. (2021). Build permissioned distributed solutions and networks. Corda.net.

Deshpande, A., Stewart, K., Lepetit, L. & Gunashekar, S. (2017). Distributed Ledger Technologies/Blockchain: Challenges, opportunities and the prospects for standards. British Standards Institution.

Dinh, T. N. & Thai, M. T. (2018). AI and Blockchain: A Disruptive Integration. Computer 51(9):48-53.

Ernst, E., Merola, R. & Samaan, D. (2019) Economics of artificial intelligence: Implications for the future of work. IZA Journal of Labor Policy, Volume: 9, 2019, Issue: 1, Pages: 1-35.

European Commission. (2019). How can Europe benefit from Blockchain technologies? Digital Single Market Report.

EY. (2017). Better-working insurance: moving blockchain from concept to reality. ey.com.

Govchain. (2019). Estonia. govchain.world.

Government Office for Science. (2016). Distributed Ledger Technology: beyond block chain. A report by the UK Government Chief Scientific Adviser.

Grabowski, M., Rowen, A & Rancy,J_P. (2018). Evaluation of wearable immersive augmented reality technology in safety-critical systems, Safety Science, Volume 103, 2018, Pages 23-32.

Hileman, Dr. G. & Rauchs, M. (2017). Global Blockchain Benchmarking Study. Cambridge Centre for Alternative Finance.

Hofer, L. (2018). Blockchain and microfinance: hype or promise? Theblockchainland.com.

Huibers, F. (2021). Distributed Ledger Technology and the Future of Money and Banking. Accounting, Economics, and Law: A Convivium, 2021.

Hassani, H., Huang, X. & Silva, E. (2018). Banking with blockchain-ed big data. Journal of Management Analytics Volume 5, 2018 – Issue 4, Pages 256-275.

Leopold, T., A, Ratcheva, V. & Zahidi, S. (2016). The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution. Global Challenge Insight Report. World Economic Forum.

Mastercard. (20121). Mastercard Start Path Selects Six Fintech Innovators to Build the Future of Sustainable Lending, Blockchain-Powered Social Impact and More. Press Release. 3rd May, 2021.

Morkunas, V. J., Paschen, J., Boon, E. (2019). How blockchain technologies impact your business model,

Business Horizons, Volume 62, Issue 3, Pages 295-306.

Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System. Bitcoin.org.

Natarajan, H., Krause, S. & Gradstein, H. (2017). Distributed Ledger Technology and Blockchain. FinTech Note; No. 1. World Bank, Washington, DC. World Bank.

Ojo, A. & Adebayo, S. Blockchain as a Next Generation Government Information Infrastructure: A review of initiatives in D5 countries. Insight Centre for Data Analytics. National University of Ireland, Galway (NUIG).

Schwab, K & Samans, R. (2016). Preface of The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution. Global Challenge Insight Report. World Economic Forum.

Sundararajan, A. (2017). The Future of Work: The digital economy will sharply erode the traditional employer-employee relationship, Finance & Development, 0054(002), A003.

Tapscott, A & Tapscott, D. (2017). How Blockchain Is Changing Finance. Harvard Business Review.

Thomas, S. (2016). Illinois Blockchain Initiative. NASCIO Award Category, Emerging & Innovative Technologies, State of Illinois. Treleaven, P., Gendal Brown, R. & Yang, D. (2017). Blockchain Technology in Finance. Computer, vol. 50, no. 9, pp. 14-17, 2017.

I spent some time this week working on how we think about risk, and start to recgonise that estimating and quantifying the likelihood of a risk occurring isn’t a very helpful way of thinking about some risks. For some risks, the kind of risks where even a single occurrence is unacceptable, severity is what matters. The tendency of likelihood-focused thinking is to assume that risk can be mitigated to point of being extremely unlikely to occur, and so severity doesn’t matter. But severity-focus thinking assumes the risks of high severity are always high severity, however likely or unlikely they are to occur, and so either need to be accepted or removed entirely.

Rationalising requirements

Of course no product manager should just be taking business requirements and handing them to the development team to build without some rationalisation and validation, but I’ve been spending quite a bit of this week figuring out what a structured rationalisation process might look like with getting caught in a bootstrap problem. Our programme design teams want to add something to the courses we deliver, and that thing requires some costly and complex technical development, which we don’t want to do unless we’re sure it’s going to get used and so we ask questions about how people might be trained in using this new feature, how many people might benefit, what is the total value, but of course those are hard questions to answer with only an idea of something to add. So where to start, that is the question.

A porous membrane for the organisation, and why it matters for product thinking

I’ve been thinking for a while about how and why the boundary between an organisation and society can be made porous to allow for knowledge to flow both ways. Whether this is Friedman’s nonsense about the purpose of a company or Macleod’s ideas about how organisations use blogging and social media, or how technology products act as interfaces between organisations and customers, the nature of the relationship between organisations and society is changing.

Simple machines

I went to a launderette and used a change machine. I’m fascinated by simple machines like these that have a very direct logic about their interface and require the people using them to make the decisions. Most of the software we use is other people’s decisions.

And thought abut:

What problem does Product Management solve?

A colleague asked me about what I do as a product manager, and as usual I struggled to articulate anything more than, “whatever I can to help the product be a success”. Generally, the usual explanation of being at the intersection of technology and what we can do with it, business objectives and how we achieve them, and customer needs and how to meet them, works but doesn’t help anyone understand the what or how of product management in a charity. There’s acceptance that there are lots of overlaps with what other roles do, there’s some business analysis, technical architecture, UX design, customer support, etc., but what does product management do that is unique to product managers? Or to put it another way, what problem does the role of a product manager solve for the organisation?

Change isn’t failure

Making a decision that was right at a point in time but, having learned more since then that makes that decision now look wrong, doesn’t actually make it a wrong decision. It’s better to make a new decision based on new information. Not making a new decision, continuing with the old decision, is more wrong now than the original decision. How we frame learning and making new decisions not as failures and changing minds, but as progress and the mark of good leadership in a digital organisation is a challenge.

And I read about:

Team topologies

I listened to a podcast about Team Topologies and patterns that help organisations achieving a fast flow of change in order to be more successful at software delivery. The three key principles they talked about were: Optimising for faster flow in live systems, using rapid feedback from those live systems so teams can course correct, and limiting team cognitive load. These allow teams to assume end-to-end responsibilities and develop solid practices. I’m definitely going to learn more about this.

Rethinking the ‘rainy day’ myths of charity reserves

Charity reserves are an interesting thing. There’s a lot to rethink and and lot of perspectives to rethink from. In start-up terms, it would be called a runway. It’s how long the organisation can operate before it runs out of money. For a charity, and more so for the people who are helped by the charity, the length of that runway is even more important than for most startups. Thinking around reserves crosses-over with the financial literacy of the trustees running the charity, the appetite for risk vs. interpretations of responsibility for overseeing the correct running of the charity, the types and sources of funding available, how many people are paid employees of the charity. All of these things and more should inform each charities position on reserves. It’s a more complex calculation than blanket guidance of x number of months operating costs can cover.

Direct Acyclic Graph

DAG’s are the latest and coolest implementations of Distributed Ledger Technologies. They tackle many of the issues that the sequential DLT’s such as Blockchain suffer from (although of course have their own downsides). As interesting as the technologies are, and s interesting as the use cases for the technologies are, I think the most interesting thing is how the ideas behind the technologies are going to affect our worldviews. We haven’t even figured out how the technologies of the internet have affected us, and here we already experiencing very different concepts.

We were very close to launching a new product. We’ve been working really hard on it but it’s just not ready, and neither are our people. Some times that’s how it goes. The thing I’ve learned over the past few weeks is that product development codifies organisational complexity. It’s Conway’s Law on another level. The strengths, weaknesses, gaps and skills of the organisation will show in the product. I wonder whether it’s even avoidable.

Every organisation is going through digital transformation

Every organisation is going through digital transformation, some just don’t know it yet. I attended a board meeting where we discussed the strategy for Bucks Mind for the next two years. We’re at an interesting stage in the growth of the organisation where technology is becoming essential to it’s success. It’s a big step to take, and quite an unknown for many people in the organisation. The idea that technology solves problems, takes care of itself, increases efficiency, etc., when in fact technology increases complexity, dependency, demands more formalised skills, etc.

How and if to educate users

I had an interesting chat about educating users of a product. On one side of the argument; if you have to explain how to use the product maybe it’s too complicated, but on the other side, people don’t have time to explore every piece of functionality. Can education be a barrier for some and an enabler for others? Maybe education should help the user know what they can achieve, but then the product should help them achieve it without having to think about how to do it. Maybe it’s ‘educate for outcomes, self-explanatory for outputs’.

What is the role of DLT and blockchain in the future of work?

I picked the essay question for my assignment for the Blockchain module I’m studying. I had thirty to choose from, which I filtered down to:

How can blockchain technology change the structure and the operations of organisations?

Discuss how blockchain can have a positive impact on the UN Sustainable Goals.

Assessing the concept of Decentralised Autonomous Organisation (DAO) as a new corporate structure highlighting benefits and downsides.

What is the role of DLT and blockchain in the future of work?

…but I think I’m going to do “What is the role of DLT and blockchain in the future of work?” There should be some interesting things to think about around how smart contracts are and can be used, how necessary trust and transparency across supplier networks, and how organisations profit from digital asset ownership.

Thought about:

Solving interesting problems

The problem with not having any slack time at work is it stops us from tackling interesting problems. When faced with barriers and no time, we pick up the easier work instead in order to get stuff done rather do the tangential work to remove the barrier. This completion bias keeps us doing shallow work, work that needs to be done, but at the ultimate expense of creative work. So, more slack time at work. More slack thinking.

Who measures impact?

Funder gives charity money, charity uses money to help people (or animals, environment, whatever), charity measures impact of helping, charity reports impact to funder. That’s how it usually works, I guess. But what if funders didn’t ask charities to report on their impact but instead to enable to funder to measure the impact directly with those who received the help. Or, what if there were organisations that specialise in measuring and reporting impact that act as intermediaries between funder, charity and beneficiary? Why should it be that charities measure their own impact? Apart from any ‘marking your own homework’ issues, it probably isn’t the core capability of most charities and maybe they’d benefit more if their measurement efforts were focused on service delivery improvements.

I read:

Useful things for privacy and ethics in tech innovation