The future is already here, it’s just distributed across a decentralised network: the role of DLT and blockchain in the future of work

Introduction

It is generally accepted that emerging technologies act as enabling forces for economic, social, and business transformation (Cohen & Amorós, 2014; Paschen, Kietzmann, & Kietzmann, in press, in Morkunas et al, 2019). Morkunas et al (2019) predict that blockchain technologies will “challenge existing business models and offer opportunities for new value creation”, whilst the UK Government Chief Scientific Officer described distributed ledger technology as a “potential explosions of creative potential that catalyse exceptional levels of innovation“ that can “reform our financial markets, supply chains, consumer and business-to-business services, and publicly-held registers” (2016). If these predictions come to fruition then we can expect Distributed Ledger Technology and Blockchain to have considerable impact on business and the future of work.

This essay attempts to reach an answer to the question ‘What is the role of DLT and blockchain in the future of work?’ The question is explored through looking at recent literature for a definition of the future of work, how emerging technologies, specifically Distributed Ledger Technology and Blockchain, are expected to affect the nature of work, and which sectors are likely to be most impacted. The discussion considers examples of the use, issues and challenges for DLT and blockchain in the top three affected sectors. In drawing a conclusion about the role of DLT and Blockchain in the future of work I argue that emerging technologies have an amplified impact where more than just a single technology is applied, and that DLT and blockchain are likely to have a greater impact on some sectors than others.

Literature Review

What is the future of work?

Work in the 21st century is entering a Fourth Industrial Revolution, a revolution built on an increasing number of emerging and interacting technologies that is “more comprehensive and all-encompassing than anything we have ever seen” (Schwab & Samans, 2016). ‘The future of work’ is a current and ongoing debate about how every occupation in every sector is undergoing a fundamental transformation as a result of the impacts of emerging technologies and digital transformation. The debate is wide-ranging, with far-reaching consequences, spanning from the offer of benefits for employers and employees augmented by technology (Grabowski, 2018) to mass economic disruption from the loss of jobs (Ernst et al, 2019). While some jobs are threatened by redundancy and others grow rapidly, existing jobs are also going through a change in the skill sets required to do them (Schwab & Samans, 2016). Some sectors can expect greater change than others.

What factors will affect the future of work?

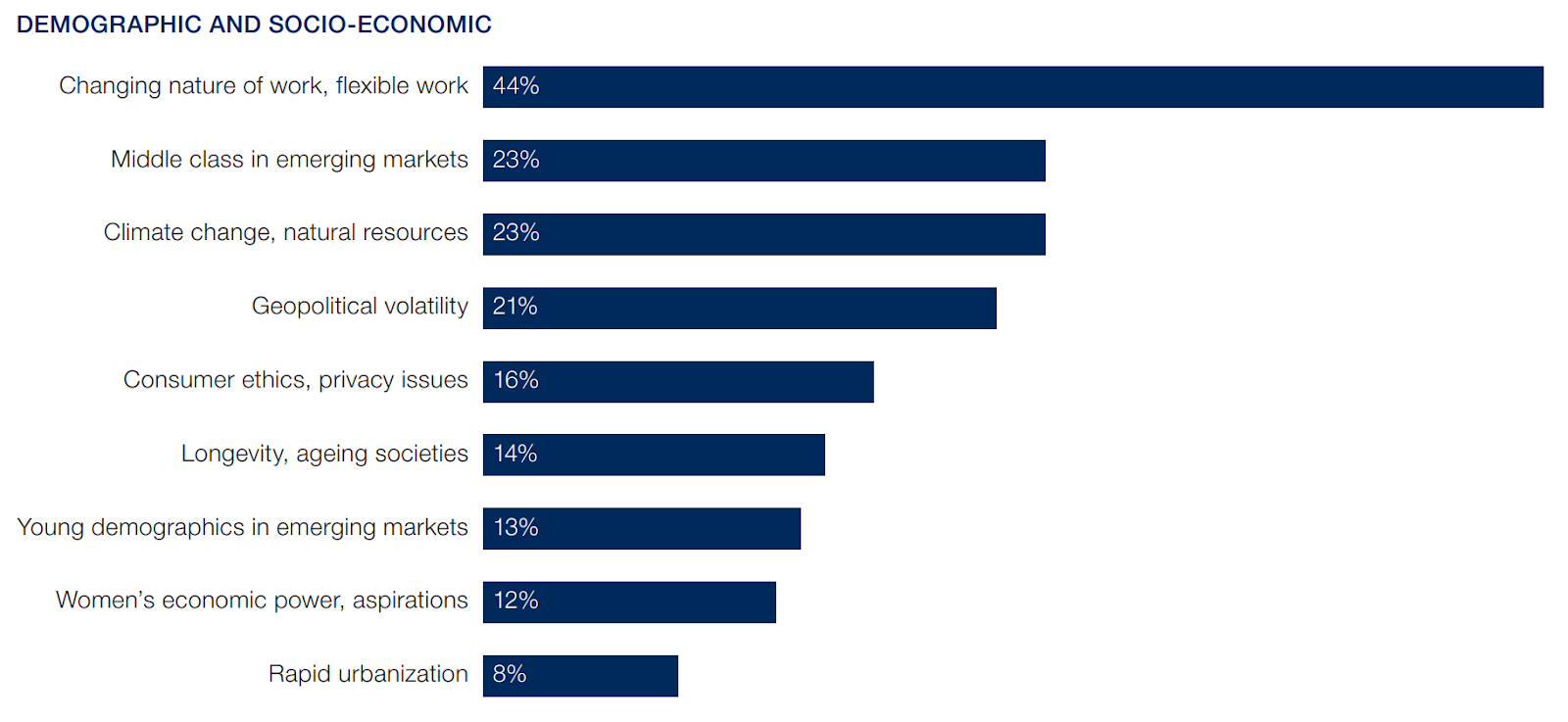

Along with the changes to work and working life brought about by technology there are wider trends such as globalisation of labour markets through the diffusion of outsourcing and offshoring, and job polarisation (Berg et al, 2018) that impact the future of work debate. For the purposes of this paper we cannot consider all of these factors and will instead focus on the potential impacts of emerging technologies in general, and Distributed Ledger Technologies and Blockchain specifically as we try to understand what role they may play in the future of work. However, one closely related trend that is worth discussing is the increase of flexible working arrangements as shown in Figure 1. The graph from the World Economic Forum shows 44% of respondents stated that the changing nature of work was the greatest driver for change across all industries. This matches with the findings from Berg et al (2018) where the two most important reasons for crowdworking were to “complement pay from other jobs” (32%) and because they “prefer to work from home” (22%). This suggests people are looking for more flexibility in their working life and turning to technology to enable it.

Figure 1: Demographic and socio-economic drivers of change, industries overall

Source: The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution, World Economic Forum.

Which technologies will affect the future of work?

The World Economic Forum report lists the nine technologies it’s respondents considered drivers of change (Fig. 2). Noticeably, DLT & Blockchain are not specifically listed as technologies that are expected to drive change. It could be argued that DLT & Blockchain technology has yet to achieve the maturity and adoption necessary for a study of this breadth to recognise its potential impact. This is backed-up by the British Standards Institution report which states the challenges of Blockchain adoption as including: “lack of clarity on the terminology and perceived immaturity of the technology, perceived risks in early adoption and likely disruption to existing industry practices, and insufficient evidence on business gains and wider economic impact” (Deshpande, 2017). DLT and Blockchain should be expected to impact the future of work, but perhaps those expectations are not arising just yet.

Figure 2: Technology drivers of change, industries overall

Source: The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution, World Economic Forum.

If Distributed Ledger Technologies and Blockchain are not yet impacting businesses and the future of work in a generic way like mobile and cloud are, then which specific industries are being affected by DLT and Blockchain?

Which sectors are likely to be most affected by Blockchain?

The Global Blockchain Benchmarking Study (Hileman & Rauchs, 2017) (Fig.3) shows how blockchain is at use by different industry sectors, with the banking & finance industry the highest user, followed by government & public goods, and then insurance. Those sectors which use Blockchain the most stand to be the most affected by its use, and so it is these sectors that we should expect DLT and blockchain to play more of a role in shaping the future of work.

Figure 3. Sectors currently using blockchain.

Source: Global Blockchain Benchmarking Study

Discussion

The following discussion looks at the role DLT and blockchain may play in the future of work in the top three sectors identified in the Global Blockchain Benchmarking Study, including examples and considering some of the challenges and issues.

Distributed Ledger Technology and Blockchain in the Banking and finance sector

The finance sector is being disrupted by DLT and blockchain (Buitenhek, 2016., Natarajan et al, 2017, Treleaven et al, 2017, Hassani et al, 2018). This seems undeniable. Blockchain technology serves a finance use case very well, offering as it does an immutable record of transactions and means of solving the double-spend problem (Nakamoto, 2008). Services such as Corda which “enables businesses in Banking, Capital Markets, Trade Finance, Insurance and beyond to transact directly and in strict privacy using smart contracts, reducing transaction and record-keeping costs and streamlining business operations” (Corda, 2021) demonstrate how large corporations in highly regulated industries are beginning to adopt blockchain technologies.

However, blockchain is not without its weaknesses of security, scalability, and efficiency (Dinh & Thai, 2018) which present considerable challenges in a banking and finance setting. Adoption of new technologies is always dependent on multiple factors, but perhaps it is precisely its disruptiveness that presents a challenge to the adoption of DLT and blockchain in the finance industry. As Tapscott and Tapscott (2017) state, the finance industry suffers from being “centralized, which makes it resistant to change… but the solution to this innovation logjam has emerged: blockchain.”

Let’s consider a case study of how one start-up is using blockchain to provide a disruptive microfinance solution.

Blockchain in Microfinance

“As the fintech landscape evolves at an unprecedented speed, Mastercard provides the infrastructure and assets to help fintech innovators grow and ultimately bring more people into the digital economy,” said Amy Neale, Senior Vice President, Fintech & Enablers. (Mastercard, 2021). One of those innovators is Brazil-based Moeda Seeds, a digital banking, payment and micro credit services powered by blockchain. “Since its founding in 2017, the company has used blockchain technology and has focused on the unbanked and under-banking population in Brazil“ (Moeda, 2021). They use blockchain technology to decrease lending costs, allowing microfinance lenders to send money directly to the recipients without the need for various middlemen (Hofer, 2018).

Microfinance Institutions, like Moeda, are organizations that provide small loans to borrowers who typically lack collateral, steady employment, or a verifiable credit history and therefore do not have access to traditional commercial banking (Coli et al, 2021). The use of Blockchain technology in microfinance introduces a number of benefits that are difficult to achieve through traditional financial institutions and technologies, including:

- Transparency for investors to monitor repayments.

- Reduced transaction fees by removing the need for intermediary organisations.

- Builds an immutable and publicly available credit history for each lender (Adebaki, 2019).

In the case of Moeda, blockchain plays a role in the future of work for the Brazilian farmers, enabling them to fund their businesses without the need for traditional finance mechanisms such as capital or credit history.

Distributed Ledger Technology and Blockchain’s role in Government & Public Goods

Distributed Ledger Technologies and Blockchain have a role to play in government by performing a range of activities, including:

- verification of documents such as licenses, proofs of records, transactions, processes or events such as birth of a child,

- movement of assets such as transferring money from one entity to another after some work conditions are met,

- asset ownership registers such as land registries, property titles and other types of ownership of physical assets and

- management of identities like e-identities for citizens and city residents. (Ojo & Adebayo)

Blockchain can be used to address inefficiencies in government systems to increase the effectiveness of public service activities (Ojo & Adebayo). An example of this can be found in the Illinois Department of Innovation & Technology’s proof-of-concept for providing physicians with a means to obtain licenses to practice in multiple states. The Interstate Medical Licensure Compact, built on blockchain, not only offers advantages for the physicians but also strengthens public protection by enhancing the ability of states to share investigative and disciplinary information (Thomas, 2018).

The challenges around government departments adopting emerging technologies such as blockchain include justifying the use of public money and whether blockchain serves sufficient use cases. Estonia has been testing blockchain for limited use cases such as land registry to improve data integrity but has clearly stated that investment in other emerging technologies such as artificial intelligence is a greater priority (Govchain, 2019).

Distributed Ledger Technology and Blockchain in the insurance industry

DLT and blockchain continue to be explored in the insurance industry as a means of achieving the vision where “data is linked automatically to digital contracts which can trigger automated processes. Everyone trusts the accuracy of the data and can share it easily. World-class encryption provides the necessary security, and there’s a clear, immutable audit trail to underpin end-to-end underwriting and claims governance.” (EY, 2017). EY’s Insurwave, a blockchain enabled marine insurance product, aims to “deliver major gains in transparency, efficiency and auditability in the insurance value chain.” (EY, 2017). Replacing traditional databases with a blockchain creates immutable records allowing for better risk assessments on the part of insurers and quicker claims payouts for shippers. The operational efficiency gained by such solutions reduces the cost of moving information within and between companies. However, an issue to be faced by the insurance industry as a whole is how to work with regulators to ensure legal requirements and regulations evolve in line with new use cases for the technology. Clearly this is a policy issue rather than a technology one but could stand in the way of blockchain solutions becoming the standard across the insurance industry.

Conclusion

This essay started with a definition of the future of work debate as a response to emerging technologies and digital transformation, and considered which sectors are likely to be the most affected by the use of DLT & blockchain. The discussion looked at the use of blockchain in the finance sector, government and insurance industry, considering some current uses, challenges and opportunities. From looking at this we can draw the following conclusions:

- DLT & blockchain will have a far greater role in changing some industries than it does in others. The effects will be greater in sectors where multiple organisations need access to the same data and for that data to be trusted as a single source of truth.

- DLT & blockchain is likely to change the nature of the relationship between businesses, transforming aspects where a trust-based relationship exists. It has the potential to enable businesses to move away from centralised authorities.

- All sectors and industries suffer similar challenges with the adoption of DLT & blockchain, including regulation, understanding and clearly defined use cases.

- The effects on the future of work are likely to be considerably more profound where DLT & blockchain intersect with other emerging technology such as the Internet of Things and Artificial Intelligence.

Distributed ledger technologies and blockchain, as two of many emerging technologies, can be expected to have a contributory role in changing the future of work, and it’s clear how these technologies can be used in specific use cases, but it would be less prudent to conclude a general direct impact in the way that automation technologies, for example, can be expected to affect employment and the types of jobs available.

References

Adebaki, B. (2019). Microfinance and alternative data meets the world of Blockchain. Blockchain at Berkeley.

Berg, J., Furrer, M., Harmon, E., Rani, U. and Six Silberman, M. (2018). Digital labour platforms and the future of work: Towards decent work in the online world. International Labour Office – Geneva, ILO, 2018.

Buitenhek, M. (2016). Understanding and applying Blockchain technology in banking: Evolution or revolution? Journal of Digital Banking, Volume 1 / Number 2 / AUTUMN/FALL 2016, pp. 111-119(9).

CB Insights. (2021). Banking Is Only The Beginning: 58 Big Industries Blockchain Could Transform. CBInsights.com.

CB Insights. (2019). How Blockchain Could Disrupt Insurance. CBInsights.com.

Coli, P., Pflueger, C. & Campbell, T. (). Blockchain Uses for Microfinance Institutions in the Water and Sanitation Sector. Inter-American Development Bank.

Corda. (2021). Build permissioned distributed solutions and networks. Corda.net.

Deshpande, A., Stewart, K., Lepetit, L. & Gunashekar, S. (2017). Distributed Ledger Technologies/Blockchain: Challenges, opportunities and the prospects for standards. British Standards Institution.

Dinh, T. N. & Thai, M. T. (2018). AI and Blockchain: A Disruptive Integration. Computer 51(9):48-53.

Ernst, E., Merola, R. & Samaan, D. (2019) Economics of artificial intelligence: Implications for the future of work. IZA Journal of Labor Policy, Volume: 9, 2019, Issue: 1, Pages: 1-35.

European Commission. (2019). How can Europe benefit from Blockchain technologies? Digital Single Market Report.

EY. (2017). Better-working insurance: moving blockchain from concept to reality. ey.com.

Govchain. (2019). Estonia. govchain.world.

Government Office for Science. (2016). Distributed Ledger Technology: beyond block chain. A report by the UK Government Chief Scientific Adviser.

Grabowski, M., Rowen, A & Rancy,J_P. (2018). Evaluation of wearable immersive augmented reality technology in safety-critical systems, Safety Science, Volume 103, 2018, Pages 23-32.

Hileman, Dr. G. & Rauchs, M. (2017). Global Blockchain Benchmarking Study. Cambridge Centre for Alternative Finance.

Hofer, L. (2018). Blockchain and microfinance: hype or promise? Theblockchainland.com.

Huibers, F. (2021). Distributed Ledger Technology and the Future of Money and Banking. Accounting, Economics, and Law: A Convivium, 2021.

Hassani, H., Huang, X. & Silva, E. (2018). Banking with blockchain-ed big data. Journal of Management Analytics Volume 5, 2018 – Issue 4, Pages 256-275.

Leopold, T., A, Ratcheva, V. & Zahidi, S. (2016). The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution. Global Challenge Insight Report. World Economic Forum.

Mastercard. (20121). Mastercard Start Path Selects Six Fintech Innovators to Build the Future of Sustainable Lending, Blockchain-Powered Social Impact and More. Press Release. 3rd May, 2021.

Morkunas, V. J., Paschen, J., Boon, E. (2019). How blockchain technologies impact your business model,

Business Horizons, Volume 62, Issue 3, Pages 295-306.

Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System. Bitcoin.org.

Natarajan, H., Krause, S. & Gradstein, H. (2017). Distributed Ledger Technology and Blockchain. FinTech Note; No. 1. World Bank, Washington, DC. World Bank.

Ojo, A. & Adebayo, S. Blockchain as a Next Generation Government Information Infrastructure: A review of initiatives in D5 countries. Insight Centre for Data Analytics. National University of Ireland, Galway (NUIG).

Schwab, K & Samans, R. (2016). Preface of The future of jobs: employment, skills, and workforce strategies for the Fourth Industrial Revolution. Global Challenge Insight Report. World Economic Forum.

Sundararajan, A. (2017). The Future of Work: The digital economy will sharply erode the traditional employer-employee relationship, Finance & Development, 0054(002), A003.

Tapscott, A & Tapscott, D. (2017). How Blockchain Is Changing Finance. Harvard Business Review.

Thomas, S. (2016). Illinois Blockchain Initiative. NASCIO Award Category, Emerging & Innovative Technologies, State of Illinois.

Treleaven, P., Gendal Brown, R. & Yang, D. (2017). Blockchain Technology in Finance. Computer, vol. 50, no. 9, pp. 14-17, 2017.